Partnership problems are ratio and proportion in a business context. Two or more people invest capital for a period of time, earn a combined profit, and then divide that profit in proportion to their investment. The formula is straightforward — but the variations in how investment and time are combined create a range of question types that catch unprepared candidates off guard.

This article builds on the ratio and proportion concepts from our Ratio and Proportion guide. Every partnership problem reduces to one key idea: profit is shared in the ratio of capital × time. Once you internalize this, every question type — simple partnership, compound partnership, sleeping partner, joining at different times — becomes a direct calculation.

In SSC CGL Tier 1, partnership contributes 1–2 questions. In Tier 2, 2–3 questions appear. In IBPS PO Prelims, 1–2 questions appear regularly. The questions are formula-driven and highly repetitive in pattern — making this a reliable full-marks topic with focused preparation.

Part 1: Core Concept — The Profit Sharing Rule

The Fundamental Formula

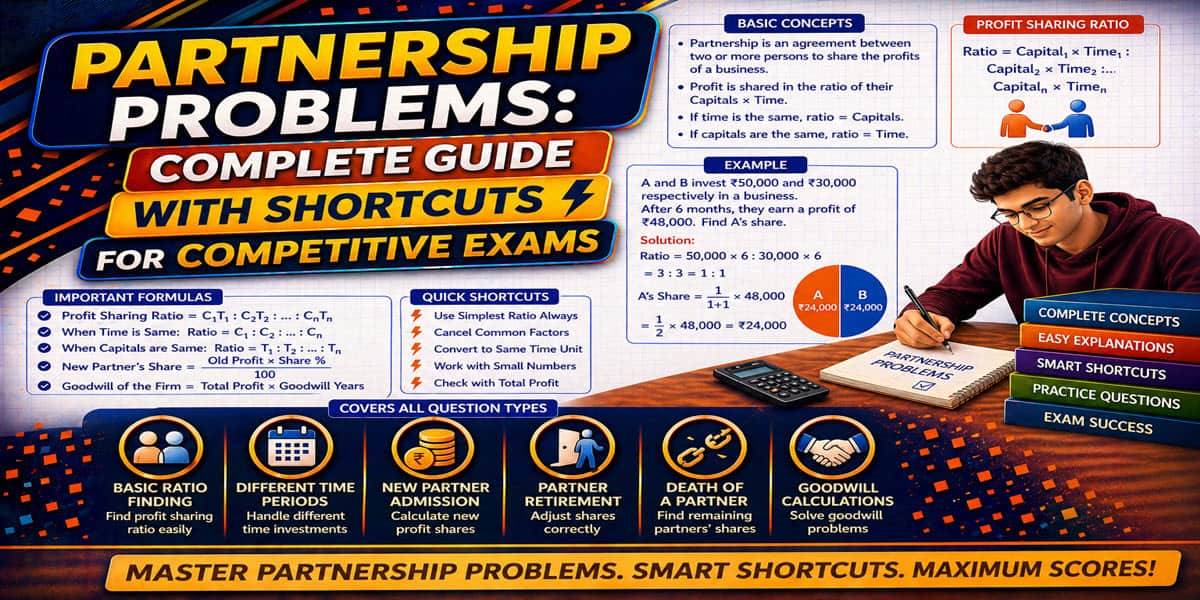

Profit share ∝ Capital × Time

For two partners A and B:

Profit of A : Profit of B = (Capital of A × Time of A) : (Capital of B × Time of B)

This single formula handles every partnership problem without exception.

Simple vs. Compound Partnership

Simple Partnership: All partners invest for the same duration.

Ratio = ratio of capitals only.

Compound Partnership: Partners invest for different durations.

Ratio = capital × time for each partner.

Part 2: Simple Partnership

All partners invest for the same time period — only capital differs.

Worked Example 1

A and B invest Rs. 30,000 and Rs. 50,000 respectively. Total profit = Rs. 24,000. Find each partner's share.

Ratio = 30,000 : 50,000 = 3 : 5

Total parts = 8

A's share = 3/8 × 24,000 = Rs. 9,000

B's share = 5/8 × 24,000 = Rs. 15,000

Worked Example 2 — Three Partners

A, B, C invest Rs. 20,000, Rs. 30,000, Rs. 50,000. Profit = Rs. 45,000. Find C's share.

Ratio = 20,000 : 30,000 : 50,000 = 2 : 3 : 5

Total parts = 10

C's share = 5/10 × 45,000 = Rs. 22,500

Worked Example 3 — Finding Investment

A and B share profit in ratio 3:4. B invested Rs. 56,000. Find A's investment.

A/B = 3/4

A = 3/4 × 56,000 = Rs. 42,000

Part 3: Compound Partnership

Partners invest for different time periods — ratio = capital × time.

Worked Example 4

A invests Rs. 40,000 for 8 months, B invests Rs. 60,000 for 6 months. Total profit = Rs. 33,000. Find each share.

A's equivalent = 40,000 × 8 = 3,20,000

B's equivalent = 60,000 × 6 = 3,60,000

Ratio = 3,20,000 : 3,60,000 = 8 : 9

Total parts = 17

A's share = 8/17 × 33,000 = Rs. 15,529

B's share = 9/17 × 33,000 = Rs. 17,471

Worked Example 5

A invests Rs. 50,000 for the full year. B joins after 4 months with Rs. 60,000. Profit = Rs. 38,000. Find B's share.

A's time = 12 months, B's time = 12 − 4 = 8 months

A's equivalent = 50,000 × 12 = 6,00,000

B's equivalent = 60,000 × 8 = 4,80,000

Ratio = 600 : 480 = 5 : 4

Total parts = 9

B's share = 4/9 × 38,000 = Rs. 16,889

Part 4: Partner Joins and Leaves — Mixed Duration

Worked Example 6

A starts business with Rs. 80,000. After 3 months B joins with Rs. 60,000. After 6 more months C joins with Rs. 1,20,000. Total profit at year end = Rs. 96,000. Find each share.

A's time = 12 months

B's time = 12 − 3 = 9 months

C's time = 12 − 9 = 3 months

A = 80,000 × 12 = 9,60,000

B = 60,000 × 9 = 5,40,000

C = 1,20,000 × 3 = 3,60,000

Ratio = 960 : 540 : 360 = 16 : 9 : 6

Total parts = 31

A's share = 16/31 × 96,000 = Rs. 49,548

B's share = 9/31 × 96,000 = Rs. 27,871

C's share = 6/31 × 96,000 = Rs. 18,581

Part 5: Sleeping Partner Problems

A sleeping partner invests capital but does not actively work in the business. The active partner may receive a salary or commission from profit before the remaining profit is divided.

Method

Step 1: Deduct active partner's salary/commission from total profit.

Step 2: Divide remaining profit in capital × time ratio.

Step 3: Add salary back to active partner's total share.

Worked Example 7

A and B invest Rs. 60,000 and Rs. 40,000. A manages the business and gets 20% of profit as salary. Remaining profit shared in investment ratio. Total profit = Rs. 25,000. Find each share.

A's salary = 20% of 25,000 = Rs. 5,000

Remaining profit = 25,000 − 5,000 = Rs. 20,000

Ratio = 60,000 : 40,000 = 3 : 2

A's share from remaining = 3/5 × 20,000 = Rs. 12,000

B's share from remaining = 2/5 × 20,000 = Rs. 8,000

A's total = 5,000 + 12,000 = Rs. 17,000

B's total = Rs. 8,000

Worked Example 8

A, B, C invest in ratio 3:4:5. A is the working partner and receives 15% of total profit as commission. Remaining distributed equally. Profit = Rs. 40,000. Find A's total share.

A's commission = 15% of 40,000 = Rs. 6,000

Remaining = 34,000

Wait — question says remaining distributed equally (not in ratio):

Each gets 34,000/3 = Rs. 11,333

A's total = 6,000 + 11,333 = Rs. 17,333

Note: Always read carefully — "in investment ratio" vs "equally" gives different answers.

Part 6: Finding When Equal Profit is Shared

Some problems ask: when does a partner join such that both partners receive equal profit?

Worked Example 9

A starts with Rs. 40,000. B joins later with Rs. 60,000. They share profit equally at year end. After how many months did B join?

For equal profit: Capital × Time must be equal.

A: 40,000 × 12 = 4,80,000

B: 60,000 × t = 4,80,000

t = 4,80,000/60,000 = 8 months

B invested for 8 months → B joined after 12 − 8 = 4 months

Part 7: Investment Changed During the Year

Some partners increase or decrease investment mid-year.

Worked Example 10

A invests Rs. 50,000 for the first 6 months, then increases to Rs. 70,000 for the remaining 6 months. B invests Rs. 80,000 throughout. Total profit = Rs. 57,000. Find A's share.

A's equivalent = (50,000 × 6) + (70,000 × 6)

= 3,00,000 + 4,20,000 = 7,20,000

B's equivalent = 80,000 × 12 = 9,60,000

Ratio = 720 : 960 = 3 : 4

Total parts = 7

A's share = 3/7 × 57,000 = Rs. 24,429

Part 8: Finding Total Profit from One Partner's Share

Worked Example 11

A and B invest Rs. 25,000 and Rs. 35,000. A's share of profit is Rs. 3,750. Find total profit.

Ratio = 25 : 35 = 5 : 7

A's fraction = 5/12

Total profit = 3,750 × 12/5 = Rs. 9,000

Worked Example 12

A, B, C invest in ratio 2:3:5. C's profit share is Rs. 8,000. Find B's share.

C's fraction = 5/10 = 1/2

Total profit = 8,000 × 2 = Rs. 16,000

B's share = 3/10 × 16,000 = Rs. 4,800

Part 9: Exam Traps and Speed Tips

Trap 1 — Time Units Must Be Consistent

If one partner's investment duration is in months and another's is in years — convert all to the same unit before multiplying.

A invests for 8 months, B for 1.5 years (= 18 months) — use months throughout.

Trap 2 — "Joins After" vs. "Invests For"

"B joins after 3 months" → B invests for 12 − 3 = 9 months (in a 12-month period)

"B invests for 3 months" → B invests for 3 months only

These give completely different ratios — read the question word carefully.

Trap 3 — Working Partner's Commission Base

Commission is always on total profit — not on remaining profit after commission.

If commission = 10% of profit and profit = Rs. 20,000:

Commission = 10% of 20,000 = Rs. 2,000 ✅

Not: 10% of (20,000 − commission) ❌

Trap 4 — Equal Profit ≠ Equal Investment

Equal profit sharing requires Capital × Time to be equal — not just capital. A partner with less capital can receive equal profit by investing for a longer time.

Speed Tip — Cancel Zeros First

When computing capital × time ratios, cancel common zeros immediately:

50,000 × 12 : 60,000 × 8 = 50 × 12 : 60 × 8 = 600 : 480 = 5 : 4

Working with smaller numbers reduces calculation errors significantly.

Quick Reference Formula Sheet

| Situation | Formula |

|---|---|

| Simple partnership ratio | Capital A : Capital B |

| Compound partnership ratio | (Cap A × Time A) : (Cap B × Time B) |

| Finding investment | Investment = ratio share × known investment / known ratio |

| Working partner total | Salary + share of remaining profit |

| Equal profit condition | Cap A × Time A = Cap B × Time B |

| Changed investment | Sum of (investment × time) for each period |

| Total from one share | Total = known share / known fraction |

Exam-Wise Strategy

| Exam | Questions | Common Types | Time Budget |

|---|---|---|---|

| SSC CGL Tier 1 | 1–2 | Simple + compound partnership | 60–75 sec each |

| SSC CGL Tier 2 | 2–3 | Sleeping partner + joining at different times | 90 sec each |

| IBPS PO Prelims | 1–2 | Compound + finding total profit | 60 sec each |

| IBPS PO Mains | 1–2 | Mixed duration + changed investment | 90 sec each |

| CAT | 1 | Complex multi-partner problems | 2 min |

2-Week Practice Plan

| Week | Focus | Daily Target |

|---|---|---|

| 1 | Simple + compound partnership + joining at different times | 15 questions, 20 min |

| 2 | Sleeping partner + changed investment + exam-style sets | 15 mixed questions, 20 min |